Here is your chance to demonstrate your ability to disentangle the most involved, contentious or just plain weird combinations of documents and to solve a puzzle in the field of documentary operations.

Dear TFP Experts, we have an unusual case in hand and we would greatly appreciate your immediate guidance.

At the request of our customer we issued a letter of credit (LC) covering an import of grain.

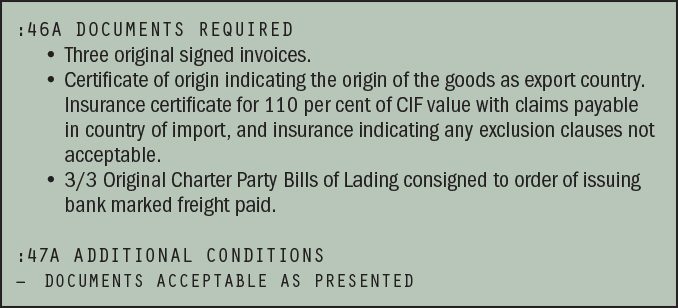

Our customer has for some time been unhappy with discrepancy fees being deducted by overseas correspondent banks and so for this latest LC the customer instructed us to include an additional condition of “documents acceptable as presented”. The justification was that this would avoid discrepancy fees.

The customer is a long-standing, reliable, creditworthy customer and we have a credit line and good collateral in place.

The LC was for US$ 550,000 covering a shipment of grain (referenced to a specific contract) but the LC did not specify the quantity of grain to be shipped, even though the separate referenced contract was quite precise in terms of quantity to be shipped.

The shipment was on a CIF basis and the LC called for the following documents (details have been abbreviated but key information is provided):

- three original signed invoices

- certificate of origin indicating the origin of the goods as export country

- insurance certificate for 110 per cent of CIF value with claims payable in country of import, and insurance indicating any exclusion clauses are not acceptable

- 3/3 Original Charter Party Bills of Lading consigned to order of issuing bank marked freight paid.

We have two urgent queries for your immediate response.

- The invoice presented was for a value of US$ 540,000 but the LC prohibits partial shipments.

- The presentation only included one document – the reference commercial invoice – without any of the other documents specified in the letter of credit being included in the presentation we received.

At our bank we are all in agreement that this is a strange situation but disagree as to whether these two items are grounds for refusal of documents.

We anxiously await your expert reply.

Solution

And the winning solution is...

Dear trade finance clinic,

First of all, the expression “documents acceptable as presented” should not be used in a credit, as this clause is not defined in UCP 600.

However, if the clause is used, its meaning should be defined in the credit – that is, the issuing bank should explain carefully its intention.

If it is not strictly defined then the definition shall have the following meaning under international standard banking practice: documents acceptable as presented.

That is to say, a presentation may consist of one or more of the stipulated documents, provided they are presented within the expiry date of the credit and the drawable amount is within the amount available under the credit. The documents will not otherwise be examined for compliance under the credit or UCP 600, including whether they are presented in the required number of originals or copies.

Typically this means that only three elements will be examined.

- At least one of the documents required by the letter of credit (LC) must be presented.

- The presentation must be made within the expiry date of the LC.

- The drawable amount must be within the available amount under the LC.

This means that the beneficiary may present only one of the documents requested under the LC, and the document examiner will only check that (i) it is the correct document; (ii) the presentation has been made within the expiry date of the LC; and (iii) the drawable amount is within the amount available under the LC.

In this particular case we do not have all the relevant data regarding the dates under the LC, but if we assume that the presentation was made within the expiry date of the credit, and we can see that the drawable amount does not exceed the available amount under the LC, then no other examination needs to be made.

Consequently, since the clause “documents acceptable as presented” has not been defined in the UCP and the issuing bank has not explained the clause in the LC terms, there is always the danger of misunderstandings and misinterpretations.

But taking into consideration the available data and according to the relevant articles in UCP 600 as well as ISBP, in my opinion this is a complying presentation.

Best regards,

Elena Ristevska

Komercijalna Banka AD Skopje

With recognition

The following readers are recognised for their technical merit

(Alphabetical order)

-

Innesa Amirbekyan

Converse Bank, Armenia

-

Nelli Kocharyan

Converse Bank, Armenia

-

Lamia Riabi

Attijari Bank, Tunisia