Here is your chance to demonstrate your ability to disentangle the most involved, contentious or just plain weird combinations of documents and to solve a puzzle in the field of documentary operations.

Our customer, the beneficiary of a letter of credit subject to UCP 600, shipped the goods by road to the place of destination and presented the documents to our bank, which we remitted as a presentation of documents to the issuing bank.

Our bank was only acting in the capacity of an advising bank, but we provided a support service to our customer by reviewing the documents before remitting to the issuing bank.

We considered that the documents on their face constituted a complying presentation and our expectation was that the issuing bank would honour the complying presentation of documents without delay.

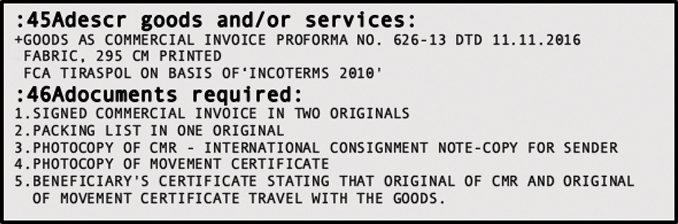

An extract of the letter of credit is included below for your guidance.

Unfortunately, the issuing bank refused the presentation and issued a “notice of refusal” stating the following two discrepancies:

“+ON CMR DELIVERY TERMS FCA TIRASPOL ON BASIS OF ‘INCOTERMS 2010’ MISSING +DISCRIPTION (QUANTITY) OF GOODS ON MOVEMENT CERTIFICATE EUR.1 DIFFERS FROM OTHER DOCUMENTS (ROLLS I/O CARGO PLACES)”

To clarify, the issuing bank rejected the documents and continues to withhold payment, first because the CMR transport document does not indicate the words “INCOTERMS 2010” and second because documents other than the movement certificate describe the goods as “cargo places”, whereas the movement certificate describes the goods as “rolls”, notwithstanding the fact that the description of the goods in the letter of credit makes no reference to either rolls or cargo places.

After some time the issuing bank returned the presented documents to our bank but the issuing bank did not make the payment under the letter of credit.

As we are all aware, the letter of credit is defined under UCP 600, article 2 as “a definite undertaking of the issuing bank”. In this current situation, the letter of credit has turned out to be quite the opposite.

We welcome the opinion of the panel of experts on this most unfortunate situation for our exporting customer who, as a small business, is striving to develop its international trade business. A loss such as this will be a major setback and shakes the customer’s confidence in trade finance instruments.

Solution

And the winning solution is...

Dear Experts,

This situation illustrates how important it is to pay attention to details when creating a notice of refusal.

UCP 600 subarticle 16 (c) (ii) states that the notice of refusal must indicate each discrepancy that is the basis for refusal. The way discrepancies are described in the refusal notice is critical.

The list of discrepancies must be complete and specific as to why the bank considers each to be a discrepancy.

In the context of the issuing bank’s refusal notice, neither of the two claimed discrepancies was clearly stated (having been further clarified by the advising bank), nor were specific reasons for determining those discrepancies highlighted.

It is also unclear whether the status of the documents was indicated.

Let us analyse the discrepancies stated by the issuing bank to determine whether they are valid.

First discrepancy: in the case of CMR we are dealing with a photocopy, which should be examined under UCP 600 subarticle 14 (f) and further clarified by ISBP 745 paragraph A6 (a). As the LC did not require the CMR to indicate the trade term or its source, the CMR need not have quoted the data stated by the issuing bank as “missing”.

No discrepancy!

Second discrepancy: the LC did not make any reference to “rolls” or “cargo places” in the description of goods. For this reason, the reference in the Movement Certificate to “rolls i/o cargo places” is not a discrepancy.

It should also be noted that in the context of UCP 600 subarticle 14 (d), the reference to “conflict with” (instead of “inconsistent with” in UCP 500) made it clear that banks should be specific in determining non-compliance due to discrepancies in data between documents.

However, in its refusal notice the issuing bank is highlighting only the difference in description of goods between the documents – without any reference to conflict between data in documents.

No discrepancy!

The discrepancies stated are therefore not valid, and as per UCP 600 subarticle 16 (f) the issuing bank is precluded from claiming that the documents do not constitute a complying presentation.

In my opinion, the advising bank should have supported its exporting customer to contest the discrepancies raised by the issuing bank and insisted on honouring the compliant presentation.

Innesa Amirbekyan

Anelik Bank, Armenia

With recognition

The following readers are recognised for their technical merit

(Alphabetical order)

Gold

-

Nina Akhremenko

Belgazprombank, Belarus

-

Aneta Cvetkovska

Komercijalna Banka Skopje, FYR Macedonia

-

Domenico Del Sorbo

Trade & Export Finance Specialist, Italy

-

Nelli Kocharyan

Converse Bank, Armenia

Silver

-

Kareem Abdel-Rahman

QNB Alahli, Egypt

-

Eissa Mohamed Eissa

National Bank of Egypt, Egypt

-

Housam Jeries Khoury

Bank al Etihad, Jordan

-

Nadezhda Khrustaleva

DemirBank, Kyrgyz Republic

-

Maria Minaeva

Deutsche Bank, Russia

-

Lamia Riabi

Attijari Bank, Tunisia

-

Elena Ristevska

Komercijalna Banka Skopje, FYR Macedonia

-

Irena Vaskov

Komercijalna Banka Skopje, FYR Macedonia

-

Ani Yeghiazarya

Ar.Medtechnica LLC, Armenia