Accessing finance in Ukraine

Thierry Senechal, CEO of consultancy firm Finance for Impact, looks at the prospects for trade finance in Ukraine

![]()

Many non-tariff barriers are negatively impacting cross-border trade.

In recent years Ukraine has experienced acute political and economic challenges.

While transition from the socialist regime started in the early 1990s and much was done to shift to a market economy, many unexpected constraints have emerged. A weak external environment, delayed structural reforms, a poor macroeconomic environment combined with the conflict in the east led to economic recession in 2014-15.

The conflict in Donetsk and Luhansk (industrialised areas with a 16 per cent share in GDP on average) has negatively affected all sectors of the economy. At the regional level, Ukraine is also largely lagging behind its neighbours in terms of economic recovery.

Trade has declined

Ukraine’s exports and imports declined in 2014-16 due to weak demand and supply-side constraints. The cumulative decline of exports was 39.4 per cent over the period 2013-15; imports fell by 62.4 per cent over the same period. Some sectors were more affected than others, for instance, machinery and equipment exports suffered from trade deterioration with the CIS market.

Historical trading relationships have been severely affected and there is no immediate sign of recovery. Historically, Ukraine imported oil and natural gas, machinery, equipment and chemicals from the countries of the former Soviet Union (for example Russia and Belarus). As a result of the conflict, the volume of trade with Russia declined from about 32 per cent of total trade in the early 2010s to 8.5 per cent in mid-2016.

Moreover, many non-tariff barriers (NTBs) are negatively impacting cross-border trade. These NTBs include: cumbersome customs procedures and long processing times for cross-border transactions; limited automation of customs operations; inadequate cross-border facilities; and limited infrastructure for providing information to the private sector.

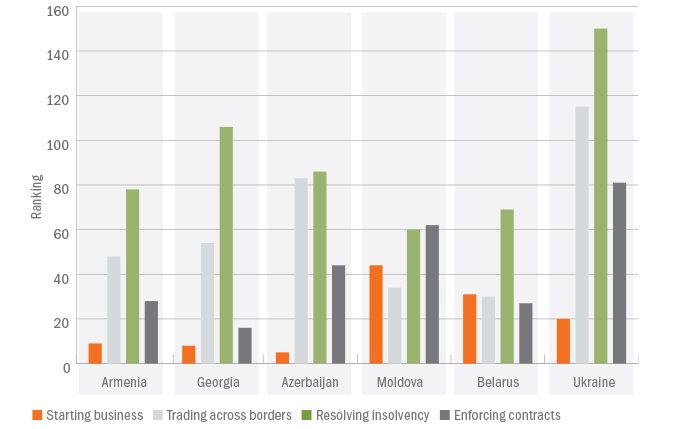

According to the World Bank’s Doing Business 2017 report, for instance, Ukraine ranked 115th out of 190 economies in 2016 on the trading across borders ranking, against 109th the preceding year. This ranking is the one of the worst in the region (see graph, below) and has deteriorated in recent years.

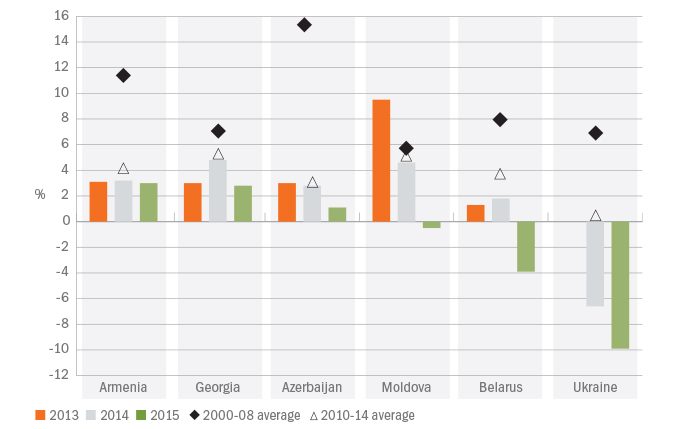

Real GDP growth in eastern European countries

Ease of doing business in Ukraine (ranking out of 190 economies in 2016)

The TFP in Ukraine in numbers

2016 saw US$ 322 million of business for some 230 transactions

Over 2,100 trade transactions worth almost US$ 2.5bn have been supported to date

Out of 24 countries using the TFP in 2016, Ukraine ranked 2nd in terms of volume of transactions

Ukraine has a competitive advantage in the agro sector

Not only has Ukraine ranked low in terms of cross-border trade performance in past years but also the country was considered “logistics unfriendly”.

The World Bank Logistics Performance Index (LPI) showed Ukraine’s ranking falling from 61st in 2014 to 80th in 2016 (out of 160 countries). The indicators relating to the efficiency of customs and quality of logistics services pointed to a worrisome deterioration in 2016. On customs efficiency, Ukraine moved from 69th in 2014 to 116th in 2016 (from 72nd to 95th for logistics services).

Lastly, enforcing contracts and resolving insolvency remain two major impediments to cross-border trade in Ukraine. According to the Doing Business 2017 report, it takes 378 days on average to enforce a contract in the case of a dispute in Ukraine at the high cost of 46.3 per cent of the claim.

Furthermore, insolvency proceedings involving domestic legal entities are time-consuming and costly. On average it takes 2.9 years in Ukraine to resolve insolvency, with the recovery rate being 7.5 cents to the dollar. Needless to say that, under these conditions, commercial banks will remain hesitant in providing financing to the real economy.

Demand

In terms of cross-border trade, there are certain areas of the economy that show promise, such as small and medium-sized enterprises (SMEs).

SMEs are best defined conceptually by their position between large corporations and informal microenterprises, with low productivity and confined to local markets.

SMEs collectively make up 99.7 per cent of all enterprises and account for about 78 per cent of all employment and 61 per cent of revenues. There were about 1.9 million companies registered in the official registry in 2015.

The most important sector of activity for SMEs is trade, followed by agriculture and then industry. These sectors account for more than half of economic activity.

Opportunities for cross-border trade are strong in the agriculture sector. Unrealised (postponed) foreign trade demand is expected to be satisfied in the coming years when current restrictions are lifted and macroeconomic constraints removed. Unused production capacities created untapped potential for growth and financing in the agriculture, food and agritech sectors.

With its low wage costs and fertile soils, Ukraine has a competitive advantage in the agro sector and access to trade financing will be important. In addition, several free trade opportunities may open up in the near future and lead to a growth in cross-border trade. For instance, the recently agreed Canada-Ukraine Free Trade Agreement (CUFTA) and the Deep and Comprehensive Free Trade Agreement (DCFTA) between the European Union and Ukraine are expected to boost bilateral trade.

2.9

the average number of years it takes to resolve insolvency in Ukraine

Supply

In the face of unprecedented political and economic challenges, the government sought to stabilise the banking sector. Recent reforms to the banking system have led to a slight increase in the performance of financial institutions. The share of assets of the largest banks has risen in past years, with the top 20 banks representing 89.7 per cent of total assets in mid-2016, thus showing clear signs of consolidation in the banking sector.

In addition, profitable trading operations have improved the financial results of many banks in recent months.

Despite liquidity in the banking sector, lending to the corporate sector is still rather conservative. Lending will remain limited unless banks clean up their balance sheets and fully disclose the real quality of their assets.

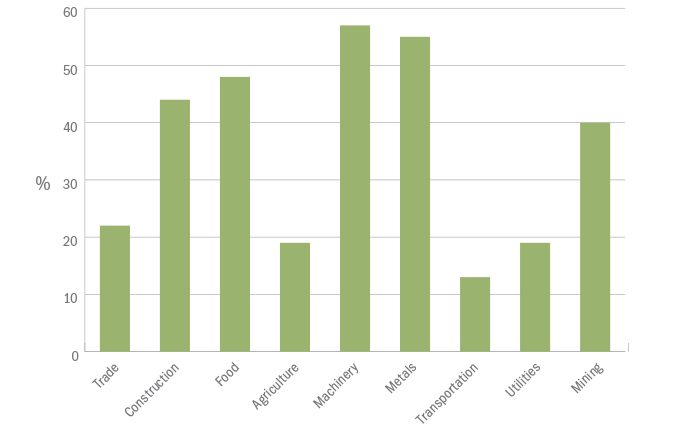

Recent evidence shows that the ratio of impaired loans increased from 10 per cent in 2013 to above 30 per cent in 2016 (the rate of NPLs reported by foreign banks in the third quarter of 2016 is 37.5 per cent, and 44.2 per cent for public banks). The level of default on loans remains very high in some sectors. For instance, in the trade sector, the share of NPLs is about 22 per cent of the total portfolio, with worrisome performance in the machinery and metals sectors.

Share of non-performing loans (March 2016)

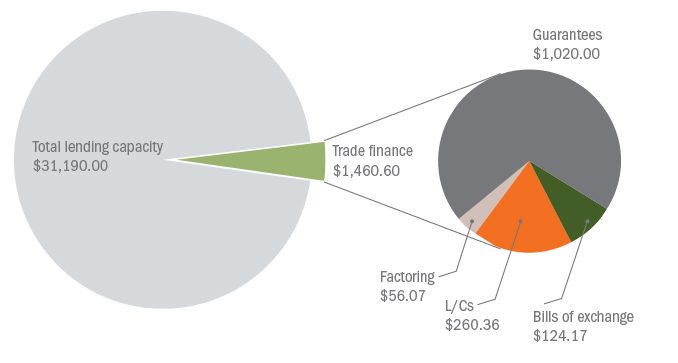

Ukraine’s total trade finance portfolio remains too small. As of 1 May 2016, the total amount of loans provided to business in Ukraine amounted to US$ 31.19 billion (UAH 777.85 billion). The trade finance portfolio (letters of credit, guarantees, avalised bills of exchange and factoring) accounted for only 4.71 per cent of total lending capacity (US$ 1.47 billion or UAH 36.6 billion). The share of trade finance out of the total loan portfolio was abnormally low for a country willing to engage in a sound export strategy over the years to come.

Who provides trade financing?

The main providers in Ukraine are: Ukreximbank (state owned); Prominvestbank (subsidiary of a foreign bank); Raiffeisen Bank Aval (majority owned by Raiffeisen Bank International and the EBRD); Oschadbank (state owned); Alfa-Bank (ABH Holding Luxemburg); PrivatBank (privately owned); First Ukrainian International Bank (privately owned); Credit Agricole (subsidiary of a foreign bank); OTP (subsidiary of a foreign bank); and VTB (subsidiary of a foreign bank).

These 10 banks hold a joint share of 77.5 per cent of the overall trade finance portfolio in Ukraine. Despite the demand of some corporates, the whole offering of supply chain finance is largely missing. Commercial banks usually offer traditional trade finance represented by letters of credit and guarantees for corporates with a sound credit history.

Other financing and risk mitigation techniques that would support trade and financial flows along end-to-end business supply and distribution chains, domestically as well as internationally, are limited.

Share of trade finance in Ukraine (US$ million)

For instance, international factoring is in high demand by traders but is largely unavailable. The international factoring mechanism is perceived as a good working capital solution for smaller corporates that could not access traditional bank finance. This mechanism allows a small business to draw money against its sales invoices before the customer has actually paid. By outsourcing the credit function, SME exporters could therefore convert the high fixed cost of operating an international credit department into a variable expense.

Although a number of banks have tried to offer factoring services to their clients, factoring accounted for less than 1 per cent of total bank lending. The lack of a robust framework is considered a major constraint for developing international factoring.

Furthermore, the cost of funding is an important obstacle to cross-border trade in Ukraine. Although the banking sector is fairly liquid, the cost of finance remains high, with evidence of credit terms in foreign currency ranging from a peak of 27-30 per cent in mid-2015 to 18-19 per cent in mid-2016 (and fluctuating at around 10-12 per cent in foreign currency for local companies).

At the peak of the crisis, the central bank raised the country’s key interest rate to about 30 per cent to stem the decline of the hryvnia and stabilise money markets, but this led to an almost complete shutdown of lending (interest rates above 40 per cent were applied to SMEs, in particular the ones not showing good creditworthiness). The use of financial and non-financial collaterals (for example, mortgages or pledges of real estate or financial assets, and cash) is another deterrent to cross-border trade.

As a result, the trade finance gap is significant in monetary terms, in particular for credit-constrained SMEs. The value of rejected transactions remains high, in particular for SMEs. It is estimated that about 40 per cent of the demand for trade finance is rejected on average, with anecdotal evidence suggesting that several financial institutions do not want to take on any risk of trade finance transactions for smaller firms.

Overall, commercial banks are clearly selective in terms of risk, as they focus on larger corporates and larger ticket transactions. The share of SME business for most foreign banks is below 10 per cent of the bank’s total portfolio. Not surprisingly, Ukrainian SMEs typically use open account terms for exporting and importing goods and services.

The international factoring mechanism is perceived as a good working capital solution for smaller corporates that could not access traditional bank finance.

Conclusion

Market failures, notably in financial markets, fell disproportionately on Ukrainian SMEs in recent years, resulting in credit rationing, high funding costs and limited use of trade finance. While the banking sector is populated with several banks that possess experience in short-term financing techniques, there is clearly a deficit of affordable trade finance and working capital targeted at SME exporters and importers.

Still, looking forward, and assuming that access to finance constraints can be removed, the existing export sector seems well placed to play a more constructive role in economic diversification.

Find out more

Thierry Senechal conducted a trade finance diagnostic study for the World Bank in 2016. Most of the data and key background material are extracted from this study.

www.finance-for-impact.com